‘My place is full, but I have no idea if I’m making enough money.’ This is one question that may have often hit you. As a restaurateur, you need to be able to analyze your daily profits and losses quickly. A restaurant’s balance sheet takes daily losses and earnings into consideration and indicates its growth percentage.

The growth percentage should include earnings, the number of guests arriving, the problems, the current assets, and liabilities. Let’s dig in to understand your restaurant’s balance sheet.

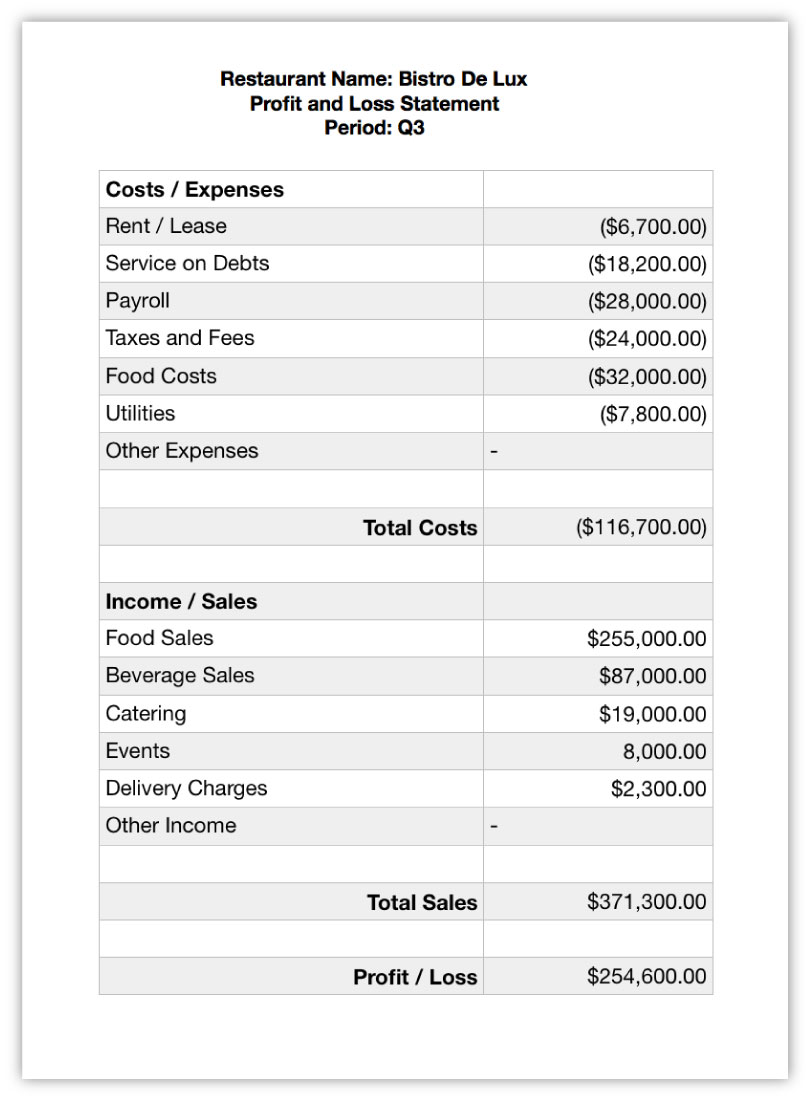

Understanding Your Restaurant Balance Sheet

Your restaurant’s balance sheet shows you your net worth in terms of assets and liabilities. You see the ‘balance’ between income and expenses, which is why it’s called a ‘balance sheet’ in the first place. Restaurateurs wanting to scale their restaurant need to be up to date with their balance sheets.

One basic mathematical formula you need to keep in mind is for your assets. It’s the sum of your equity and liabilities.

Assets= Liabilities + Equity

Assets are what your restaurant owns or generates revenues from, like equipment, inventory, cash in hand, etc.

Liabilities are expenses and outstanding bills of your restaurant, including property rent, any loans, or vendor bills.

Restaurant equity is the division of ownership between you and any partners or investors.

Calculating your balance sheet is a multiple-step process. The first step is to note down all your assets and liabilities in one place. Subtract your liabilities from your assets, and there you have your net worth.

A negative net worth indicates that your restaurant owes more than it earns. What you need to understand is that the first few months will always be hard for your restaurant. Net worth might constantly be negative. However, with constant growth and positive revenue generation, your balance between assets and liabilities will stabilize!

If you have just started to look at your restaurant’s accounts, you probably would need to be more familiar with some terms related to your balance sheet. Now, one thing you need to understand here is that the scale of your brand decides the complexity of your balance sheet. In cases of complex calculations, it is always beneficial to use restaurant management software with your spending, earnings, and so on.

Here’s a list of your different assets and liabilities for your restaurant.

Assets:

Sales

Salaries

Employee Benefits

Occupancy

Depreciation

Interest

Other income

Liabilities:

These can be further divided into two segments based on their term, current responsibilities, and long term liabilities. Another difference between the two is that the long term liabilities are not familiar to all restaurants.

Current Liabilities:

Short term loans

Utilities

Lines of credit

Income tax deductions

Medical plan payments

Property rent

Equipment

Employee salaries

Long term Liabilities:

Any long term lease

Deferred revenues

Capital leases

Equity

Leveraging Your Balance Sheet

A smart restaurant management software gives you real-time updates about your sales, your growth, the purchase orders made, and thereby the changes in your balance sheet. Analyzing your restaurant’s financial health now and then helps you make better pricing decisions. You can make early predictions of your sales trends based on consumer behavior.

Takeaways For The Restaurateur

Once you understand how to calculate your balance sheet accurately, make sure that you take care of these two things!

i) Never Track Expenses From Multiple Sources: Checking your balance sheet from multiple sources can only create more confusion. Since numerous factors come into the picture while correctly analyzing the balance sheet, you need to trust one source and stick to it. Using your restaurant POS for the same can be your best bet!

ii) Check Your Reports Daily: A lot of restaurateurs have agreed that timely checks of their accounts lead to the prevention of any malpractices. There have been a lot of times when restaurateurs feel that the restaurant is doing well without checking their balance sheet, and therefore face considerable losses in the later run.

All in all, your restaurant’s balance sheet gives you a clear understanding of your restaurant’s financial health. Keeping a regular check on it helps you make better decisions at your restaurant.